The Rise of FinTechs in India

FinTech is the culmination of “finance” + “technology” and when any business / consumer uses technology to improve their financial services, it is FinTech. The word FinTech was earlier used only for digital payments. Now, it covers a wide array of services to automate – banking services, payments, investments, trading, insurance and everything related to financial services.

Over the last decade, FinTech start-ups have become the disruptors and have started to compete with the traditional banking channels. Let us look at some of the data points to understand this point:

India has ~600 mn smart phone users, having access to multiple apps like Whatsapp, PayTm, Google Pay, etc. All these are the new mediums to make payments for personal as well as business purposes.

Number of Phone Pay, Google Pay users have crossed 175 million users

Next is the introduction of UPI based payments developed by National Payments Council of India (regulated by RBI) in 2016.

During the month of March 2021, ~USD 69 billion and since April 2016, ~800 billion worth payments were done through UPI mode.

~ 30% of retail spends are now through digital means using payment infrastructure like UPI and digital wallets (~450 million users).

These payment wallets have on-boarded ~35 million merchants on their platform and have widened digital payment network.

Retail digital lending in India has grown at a CAGR of 43%: from ~USD 9 billion in 2012 to ~USD 110 billion in 2019. It is expected to reach USD 350 billion by 2023!

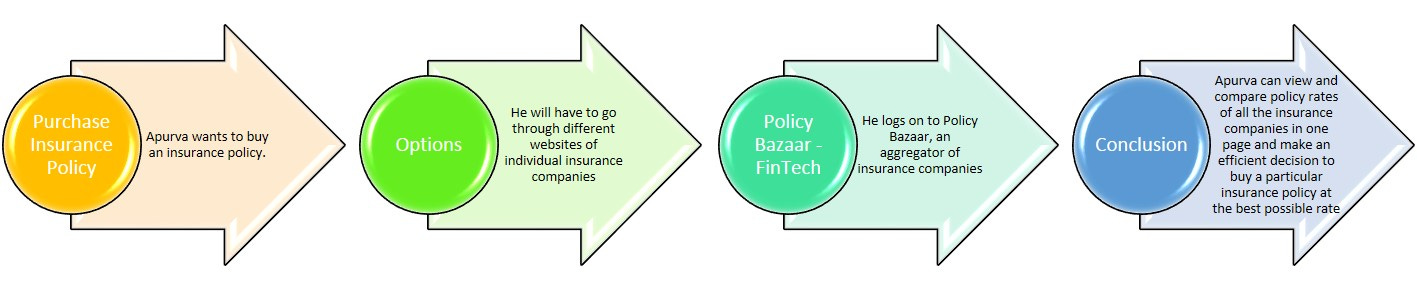

Started in 2008, Policy Bazaar is India’s largest insurance web-aggregator, having ~ 50% market share in the online insurance space.

FinFact: India has more than 30 unicorns as of today with valuation of these unicorns upwards of USD 90 billion. India is positioned 3rd in terms of value (unicorn valuation) as well as volume (number of Unicorns) behind USA and China. Within these Unicorns, ~ 30% are FinTech firms! (PayTm is valued ~USD 16 billion currently)

What led to the surge of FinTechs in India?

An easy answer is ease of doing business (commercial) or ease of doing transaction (personal finance) at a click of few buttons. Let us understand with an example:

Along with the ease of doing transactions, as mentioned earlier, the number of smart phone mobile users have increased, especially amongst millennial. As a result, the amount of data available to analyze the spending trends has increased manifolds. This data (Big Data) is available through various sources:

Online Payments

Online Shopping / POS payments at store

Entertainment

Travel Patterns

Eating Patterns

Availability of such data has helped the founders of the FinTech firms in understanding the consumer behavior very well which the traditional banks / financial services could not initially.

FinTech segmentation:

Now this leads us to the next question on how is FinTech segmented? Well, some of the different segmentations are as under:

Payments / Wallets:

Digital Lending: Online lending platforms

Digital Lending Platforms - P2P Lending, Pay Day Loans, Short Term Consumer Loans InsurTech: Online insurance platforms

Wealth Tech: Platforms that enable stock broking or provide robo-advisory services

Merchant Payments / Payment Gateways / POS: Digital payment platforms

Fund Raising:

FinTechs have been the leaders in the Indian unicorn landscape. ~ USD 10 billion has been raised by Indian FinTech firms in the last decade of which majority have been raised by payment companies and digital lenders.

Future of FinTechs in India:

FinTechs initially started as competition to the banks and financial institutions. However, over the last few years, they have realised it is better to collaborate and work together. Today, most banks work in partnership with 3-4 FinTech firms like IDFC First has partnerships with Zerodha for stock broking platform. Rupeek a Gold Loan finance company has partnered with Federal Bank, Catholik Syrian Bank and so on and so forth.

Lastly, Neo Banks are the digital-only banks, offering the entire gamut of banking services (online) to their customers. This is the new trend in the FinTech space. An example in this is Niyo (https://www.goniyo.com/) offering the following:

Savings and Wealth Management services (NiyoX),

In partnership with Equitas Small Finance Bank and with IDFC First Bank (savings account)

Forex Services (Niyo Global),

In partnership with DCB Bank

Wealth Management (Niyo Money),

Own Platform - Goalwise

Business and Salary Pre-paid Card (Niyo Bharat)

To conclude, FinTech has become a disruptor in the way traditional finance used to be practised and new forms of FinTechs are evolving each passing year. With the growing Gen X / Z population, adaptability of digital technologies amongst Indian consumers and a collaboration with the traditional banking channels - the new age FinTech firms is the future of consumer banking.

Please do drop in your comments on the article in the link below:

Second lastly, do not forget to share the article with your friends and family!

And lastly, do subscribe to FinFacts! :-)