New Age Digital Lending

In my previous article, I discussed how the FinTech market has evolved in India and is growing at an exponential rate. One of the major components of FinTech is digital lending.

The retail digital lending in India has grown at a CAGR of 43% i.e., from ~USD 9 billion in 2012 to ~USD 110 billion in 2019. It is expected to reach USD 350 billion by 2023! Such a growth has been enabled by more than 1,100 digital lending platforms in India.

Why has the digital lending gained so much traction?

This is mainly due to limitations of the traditional lending route which are:

High cost of acquisition of a customer

Requirement of physical verification

Requirement of credit history / proof of income for underwriting process

What did these limitations of the traditional lending create?

Tech enabled digital lending platforms with

Reduced borrowing cost by reducing informal lending channels

Meeting unmet credit demand by reaching out to the consumers in Tier 2 / 3/ 4 cities through smart phone penetration

Overall, achieve financial inclusion

FinFact: As on end of Feb 2021, India had 61.6 million credit cards and 894 million debit cards. Yet there are only about 3 credit cards for every 100 people in India, when compared to 32 cards in the USA. This shows that there is higher penetration opportunity in India.

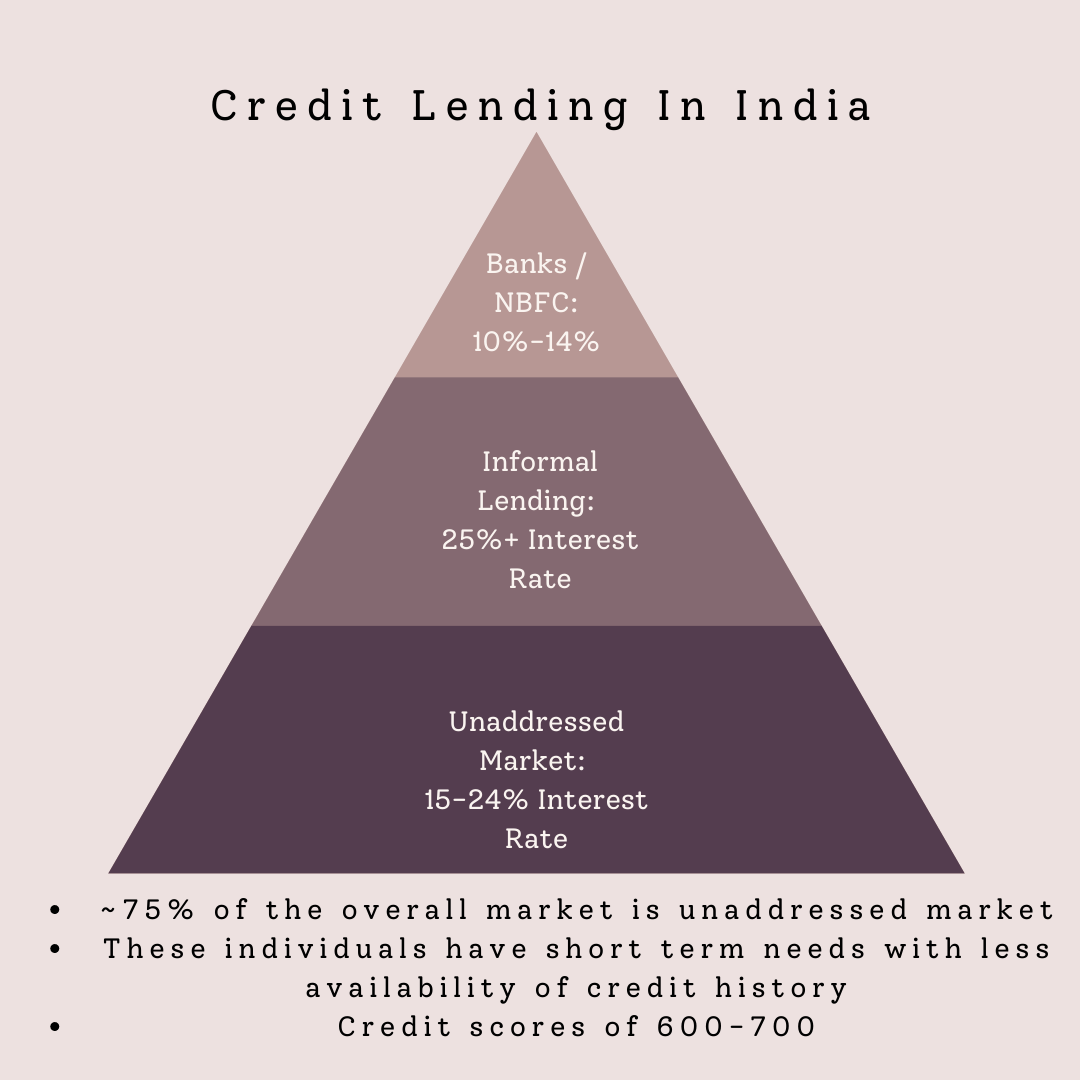

The chart below shows the credit lending market in India and the unaddressed market is what the digital lending platforms are trying to capture:

Types of Digital Lending Platforms:

Short-term lending – short term tailored loans such as payday loans, consumer loans for retail, electronic and travel expenditures etc. for instant purchases.

P2P lending –

market place model

borrowers and lenders are connected through a platform, allowing access to loans to borrowers at affordable costs.

The lending is done based on risk profiling and credit assessment by the platform.

Point-of-sale (PoS) lending –

A partnership with lenders where players finance online purchasers by using

conventional (bank statement) and

non-conventional (online purchase history) data

Pay Day Loans:

A short term + unsecured + small loan given to borrowers

Mainly salaried people borrow such loans to meet their ends meet.

It is typically for 7 to 60 days and at a very high interest rates – upwards of 30%

Loans as small as INR 3000 (USD 40)

Invoice-based lending –

An option to businesses to finance against outstanding trade receivables and securitize account receivables to improve liquidity.

Pay Later Loans –

Lenders that disburse instant, small-ticket sized loans with the ‘buy now and pay later’ model for meeting customers’ purchases.

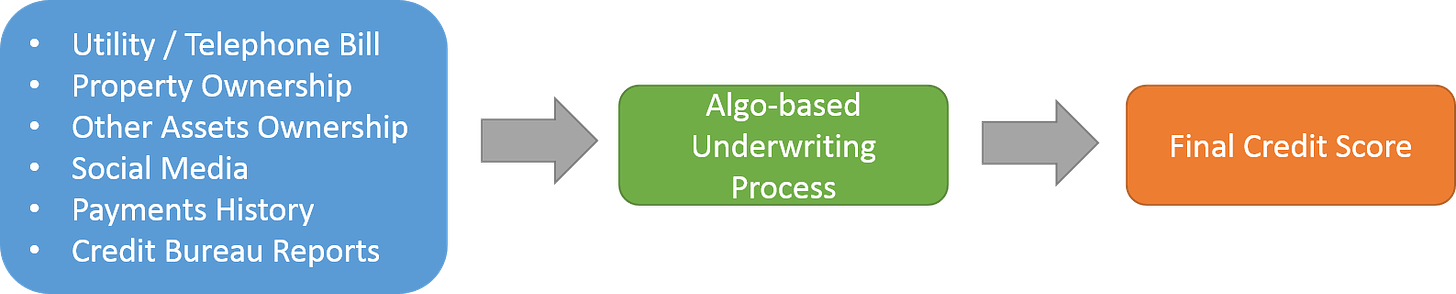

Credit Assessment:

How do these digital lenders do the credit assessment of their customers?

India has ~ 950 million mobile user network and growing + another growing credit and debit card user base of ~ 50 million. + the social media user base is ~ 270 million. This itself presents ample data

Apart from the traditional methods like the credit scores from CIBIL, Experian etc, an alternative credit scoring method is used by these digital lending platforms:

Trends to Watch Out for:

Blockchain-enabled digital identities holds immense potential. It will help to streamline the KYC process in the lending industry, thereby improve the ease of transacting. Blockchain will also help in creating centralised KYC platforms. Indeed, this is an exciting space to be in with more and more innovations / new products being introduced in the system. Until then…

Please do drop in your comments on the article in the link below:

Second lastly, do not forget to share the article with your friends and family!

And lastly, do subscribe to FinFacts! :-)

Great post! Isn’t KYC and risk monitoring centralized in India? If so, I’m sure that would also significantly cut some operational costs and barriers to entry for lending fintechs