Miracle of Compounding

On an average, 4-5 million new demat accounts are added in India each year (since 2018). This number was a whooping 10.7 million new demat accounts (more than double the average) for the period April 2020 to Jan 2021. All thanks to the volatility in the stock market due to the pandemic, more and more people are inclined towards the stock market for trading and investment purpose.

The euphoria was largely due to the recovery which was seen in the markets. After loosing ~ 32% in a span of few days in March 2020, the Nifty 50 returns from the lows of March 2020 to the end of year 2020 (24th March 2020 to 30th Dec 2020) were ~83%. This massive rally in the stock markets was driven by record foreign institutional investors pumping in ~ USD 37 billion into the equity markets (in FY21) and an expectation of stronger corporate earnings post the pandemic.

Now the question is, can an investor expect such kind of returns on a year-on-year basis?

The simple answer is NO.

The long-term average Nifty 50 return over a period of last 20 years (June 2001 to June 2021) is 13.9% and an investor, if invested only in Nifty 50 for these 20 years, would have enjoyed this compounded return of 13.9%.

Hence, Rs. 10,00,000 (Rs. 1 million) invested in June 2001 would have been Rs. 1,35,66,352 (Rs. 13.5 million) as on June 2021, a whooping 13.5x growth of principal! Now, this is the miracle of compounding.

Simply put, it is interest on interest!

How does the miracle of compounding work?

The miracle of compounding works by growing your wealth exponentially. The interest earned is added back to the principal amount and then reinvests the entire sum to accelerate the earning process.

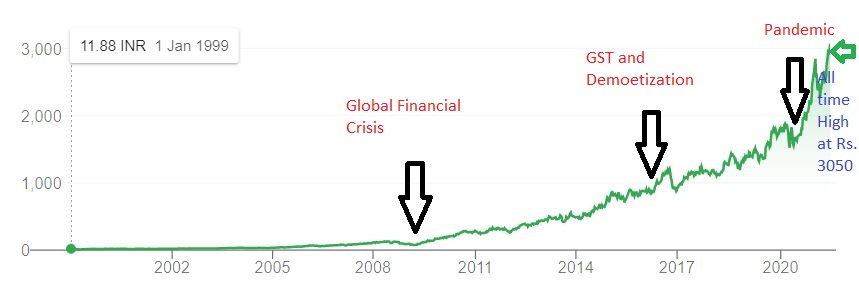

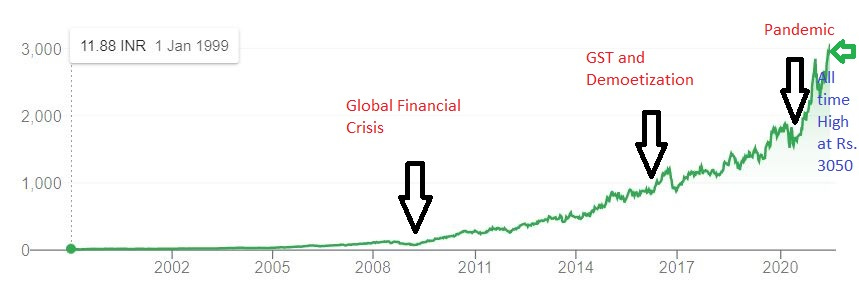

Let us understand with another example of a particular stock – Asian Paints.

The share value of Asian Paints was Rs. 11.88 on 1st January 1999. It is Rs. 3050 now as on 18th June 2021. Even without taking into account the dividends (which is ~1% for Asian Paints), the stock price has given a compounding returns of 28% in these 21 years!.

Now let us compare with the lows of 2008-09 global financial crisis. Asian Paints was trading at Rs. 79.82 on 20th February 2009 and has given compounded return of 20.7% to someone who was holding the stock since 1999.

We have gone through various crisis in between like global financial crisis, current pandemic, rise in crude oil, implementation of GST (GST on paints was highest then), thoughts that demonetization will lead to lower spends on re-painiting, and the likes. But an investment in a quality script leads to a great compounding story over the years.

Asian Paints chart since 1st Jan 1999 till 18 June 2021

FinFact:

Mr. Warren Buffet started investing when he was 10 years of age. By the time, he was 30 years, he had net worth of USD 1 million. Had he not invested and spent the money in his teens, he would probably be having only say USD 100k. Today it is a whooping ~ USD 80 billion! He kept on growing his net worth at compounded rate of 22%!. A large part of his wealth was actually built after his 50th birthday, all thanks to the base which he created early on and the power of compounding later on.

In contrast, Mr. Jim Simons, founder of hedge fund Renaissance Tech, has compounded his wealth at ~ 66%, far higher than Mr. Buffet. But Mr. Simons net worth is ~ USD 22 billion (72% less rich than Mr. Buffet!). The reason is Mr. Simons amassed his wealth only after he reached 50 and he did not have the base which Mr. Buffet started with over the initial years, Hence, even after compounding at 66%, he is still far away from Mr. Buffet.

Importance of Compounding:

The above example has led to a few important take-aways:

Start investing early – the longer the compounding, the higher the end value

Lesser Withdrawals – The lesser the withdrawals from the core investment portfolio, the higher the compounding effect.

Longer Time Horizon – The longer the time horizon, the larger the compounding effect.

Good investment is not earning the highest returns but consistent good returns over longer periods of time. That is when the compounding effect gives the desired results!

Hit the button below and share the article with your friends and family!

Please do drop in your comments on the article in the link below:

And lastly, do subscribe to FinFacts to receive the newsletter directly in your inbox! :-)

Very True

Nice and intresting article