Do you have a home loan and surplus funds now?

Do you have a home loan and surplus funds now?

Pre-pay or Invest?

Since the last one year, we are in a strange finance world – the central banks have world over infused liquidity in the markets leading to two effects (apart from the other effects):

Fall in interest rates – near zero in many geographies

Some of the liquidity flowing into the capital markets lead to surge in equity markets providing returns of ~85% returns since the fall of March 2020.

Now, this has led to a different sort of dilemma for those who have an existing home loan. I have considered only home loan and not any other type of loans like car loan or electronic goods related loan as home loans are much higher in value compared to the other loans. The question which many have in their mind is should they prepay the home loan or invest the available funds in debt or equity markets.

Obviously, there is no simple solution to this dilemma. On one hand, the home loan interest rates are as low as 6.8% and compared to that, the equities (Nifty Index) on long term basis, have given ~13.5% return over the last 20 years.

Let us discuss why the home loan should be pre-paid now:

Liability: Home loan is a fixed liability (EMI: which includes interest + principal. Interest component reduces over the life of the loan) and a burden to repay is always there. To get a peaceful sleep, it is prudent to keep the loan liabilities to the minimum or Nil.

Equity Value in Property: Through pre-payment of home loans, the borrower is increasing the equity value of the property purchased and reduces the future liabilities of interest / principal pay-outs.

Future Investments: With less debt burden in nature of home loan (lower interest + lower principal liability), the future investments can be much higher.

Tax Break: A maximum deduction of INR 150,000 from gross income is available under prevailing Income Tax rules for principal repayment of home loan. A significant part of existing EMI will also have principal payment which will also be covered under the income tax deduction. However, this option needs to be kept in mind while making the decision on the quantum of pre-payment.

If someone has any other loan with interest rate higher than the home loan interest rate, the loan with higher interest rate should be pre-paid first.

Now let us also discuss why the home loan should NOT be pre-paid now:

Guaranteed Returns:

The equity markets have given stellar returns over the years, but they are not guaranteed returns (Equity investments are subject to market risks).

If someone is looking at investments only in fixed income products, say a fixed deposit, then the returns are as low as ~5-6% for a 5 years deposit tenure.

Power of Compounding: With no / part pre-payment of home loan, the net investment (post household expenses) will be much higher and will lead to compounding benefits and in turn lead to higher pre-payment of loan at a later date.

Tax Breaks: The interest component of Home Loans provides a maximum tax break to the borrower up to INR 200,000 (Rupees Two Lakhs) each financial year. Hence, it is prudent to maintain a home loan balance of ~INR 30,00,000 (Rupees Thirty Lakhs) at interest rate of 6.7% p.a. to take advantage of tax break on interest on home loans as per the prevailing Income Tax rules. An additional maximum tax deduction of INR 150,000 (Rupees One Lakh Fifty Thousand) is available under section 80EEA of the Income Tax Act for home loan taken on affordable housing.

Prepayment Penalty: The borrower should ensure that there are no pre-payment penalties attached to pre-paying Home Loans. If there are any such clauses in the loan agreement, the cost of pre-payment of loanwill increase.

FinFact: Rule of 72: The rule of 72 is used to estimate the number of years required to double the invested money at a given rate of return or estimate the rate of return required to double the invested money over a given number of years.

Formula: Time = 72 / Rate of Return

For example: It will take 6 years for monies to double at 12% rate of return.

It is not a simple decision to pre-pay an existing home loan v/s investing the monies in debt or equity market. This decision is based on several factors like

the age of the individual,

the taxation aspect,

the overall risk profile of the borrower, etc.

Apart from the above, the key decision can be based on the following two criteria’s:

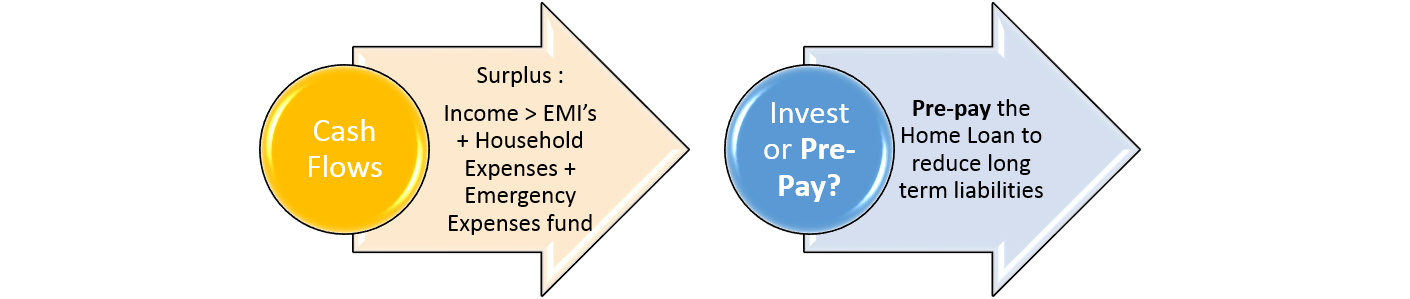

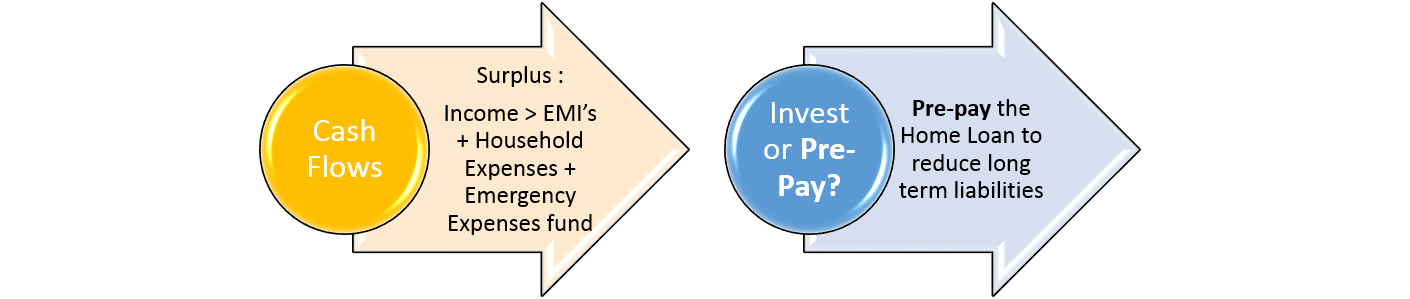

Cash Flows:

If there is surplus in Cash Flows (Income > EMI’s + Household Expenses + Emergency Expenses fund), then can pre-pay the Home Loan to reduce long term liabilities.

If there is deficit in Cash Flows (Income < EMI’s + Household Expenses + Emergency Expenses fund), then utilize the emergency expenses fund

If there is break-even in Cash Flows (Income = EMI’s + Household Expenses + Emergency Expenses fund), then no action needs to be taken

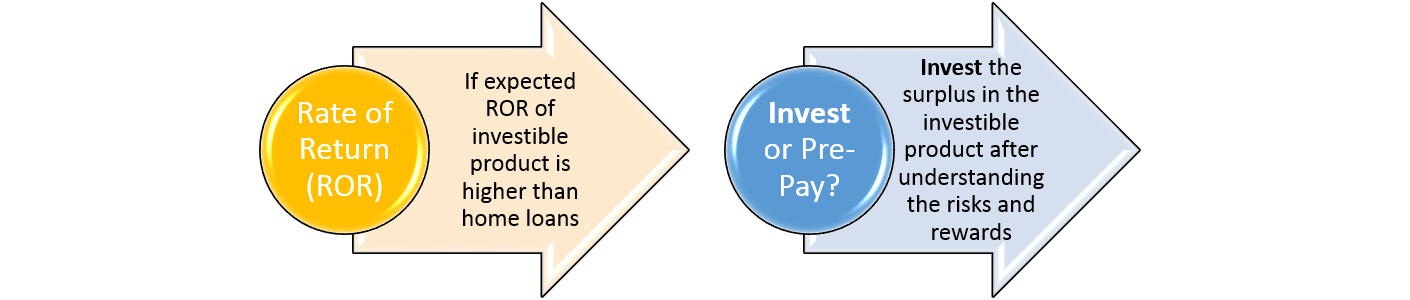

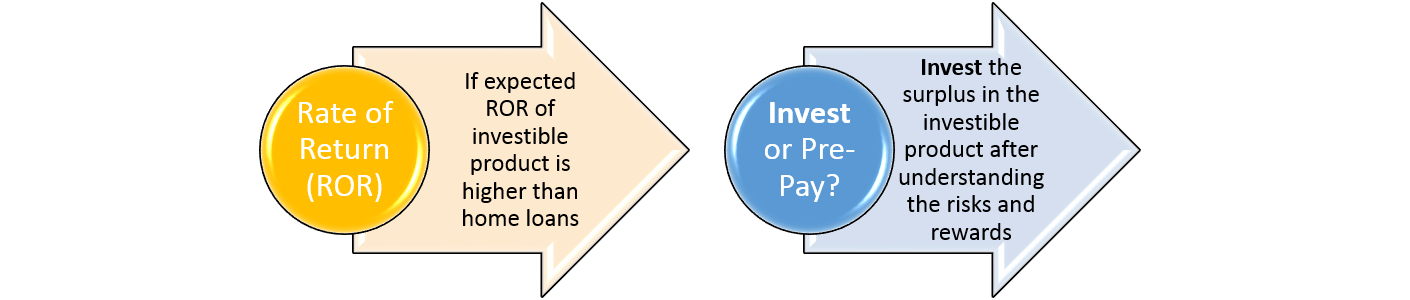

Home Loan rate v/s Investment returns rate:

Both the options – pre-pay or invest have their pros and cons and one should evaluate all possible outcomes and possibilities before reaching a decision on the next steps. Until then..

Hit the button below and share the article with your friends and family!

Please do drop in your comments on the article in the link below:

And lastly, do subscribe to FinFacts to receive the newsletter directly in your inbox! :-)