Buy or Rent?

Hey! Congratulations on your new house! That is something which most of us would hear when we buy our “dream home”. That is an aspiration which we want to achieve at some point of time in our lives. At that point of time, another thought runs through – whether to invest lumpsum into buying a real estate property or to simply rent it out. This decision is based on two important but contrasting aspects – a financial decision as well as an emotional decision.

Emotional Aspect: There is always a sense of pride in owning your own house. There is a saying that one should have – “roti, kapda and makan” (food, clothing and shelter) as a base minimum requirement for survival and hence, shelter which is your home becomes a very important aspect in overall scheme of things.

Financial Aspect: Buying a property requires a minimum of 15-20% upfront payment, if buying through a loan or 100%, if an outright buy. Obviously, one creates an asset when one buys a property. In contrast, renting a property is available at only 2-3% of the capital cost of the property in India. So, owning or renting a house has lots of financial aspects to it and that needs to be understood well.

Advantages of Owning over Renting:

Advantages of Renting over Owning:

FinFact: The gross rental yield is the return on the capital investment i.e., the percentage return on the money spent.

If one buys for Rs. 10 million and earned a monthly rent of Rs. 25,000 per month, the gross rental yield would be Rs. 25,000 x 12 / 10 million = 3.0%.

The gross rental yield in some of the continents / countries:

India: ~2-3% only!

Europe: ~ 4 – 5%

African nations like Kenya: 5.5%-6%+

Now let us analyze a bit more on the financial implications of owning v/s renting with an example:

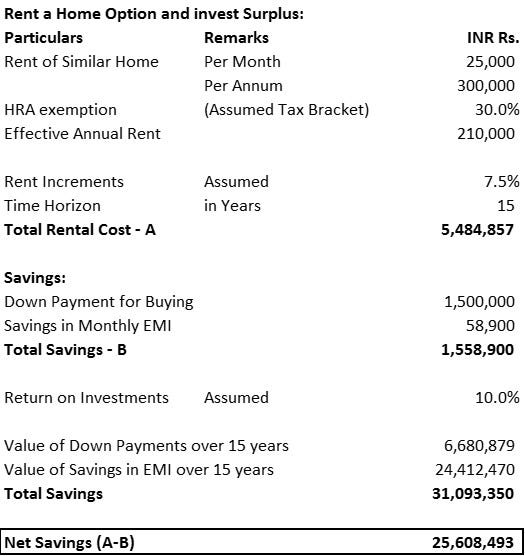

The first option is renting a house property and investing the surplus from down payments not paid and savings from EMI into certain investible products like Mutual Funds and earning a return of 10% compounding over a 15 years’ time horizon. A monthly rent of Rs. 25,000 (rental yield – 3%) is paid with 7.5% annual rental escalations. Based on the below calculations, the individual saves Rs. 2.56 crores over 15 years.

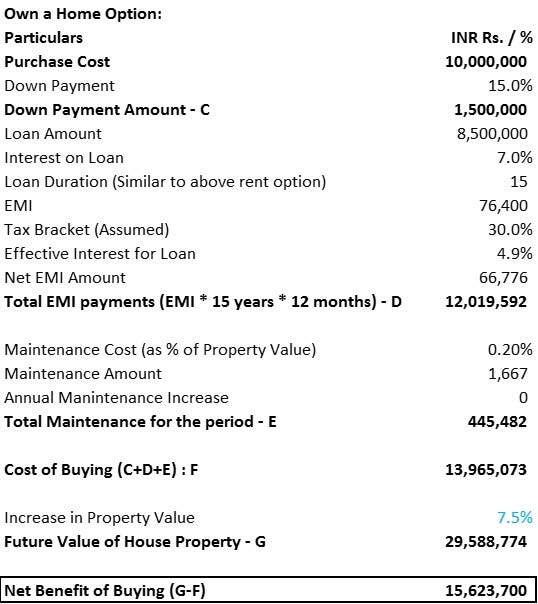

The next option is to buy a home with 15% down payment and a loan for the balance 85% at a 7% rate of interest. The cost of buying is Down Payment + EMI + Annual Maintenance Cost. It is assumed that the house property will appreciate by 7.5% per annum. Based on these below calculations, the net benefit of buying a house property is Rs. 1.56 crores

Hence, as per the above example, renting is better than owning as the savings from renting (Rs. 2.56 crores) > net benefits from owning a property (Rs. 1.56 crores).

However, the return assumption for property price appreciation is based on a number of factors. One such factor is the location of the property. In the above example, if we change the assumption of property price appreciation say from 7.5% to 10%, then owning is better than renting as the net benefits from owning (Rs. 2.78 crores) > savings from renting a property (Rs. 2.56 crores).

Conclusion:

To conclude, various factors regarding financial and emotional aspects need to be taken into consideration while making the decision on buying or renting a house. Hope you find this useful in helping you make your own.

Hit the button below and share the article with your friends and family!

Please do drop in your comments on the article in the link below:

And lastly, do subscribe to FinFacts to receive the newsletter directly in your inbox! :-)

Very nice

Very informative 🙏